Bangladesh Mobile Casino Growth and the Role of Instant Win and Crash Games

Emily Patel

Emily Patel

Bangladesh is not a simple mobile casino story. It is a collision of high mobile connectivity, massive mobile money scale, and an increasingly restrictive legal framework targeting online gambling at every layer. We spent 2025 tracking mobile casino adoption patterns in Bangladesh, and what emerged was a market shaped by contradiction.

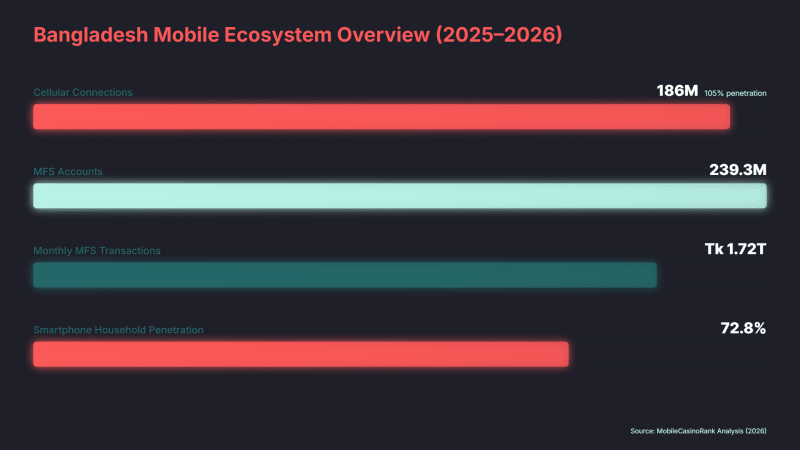

Mobile penetration is high—186 million cellular connections against a population that gives you 105% penetration. Mobile money is huge—239.3 million MFS accounts processing Tk 1.72 trillion monthly. The median age is 26, smartphone household penetration is 72.8%, and the formats gaining traction are exactly those built for mobile-first markets: instant-win and crash games. But none of that changes the regulatory reality. Online gambling is restricted under baseline statutory law, explicitly criminalized in the Cyber Security Ordinance 2025, and actively enforced through ISP blocking and payment rail disruption.

The High Court has directed BTRC to block gambling ads and ordered Bangladesh Bank to cut off MFS providers like bKash, Nagad, and Rocket from gambling transactions. This is not theoretical enforcement. It is operational and accelerating. The story we are telling here is not "Bangladesh is booming." It is "Bangladesh shows what happens when mobile-fit formats meet high-friction regulatory enforcement." The formats work. The infrastructure exists. The legal environment is the binding constraint.

This chart shows the scale of Bangladesh’s mobile ecosystem, including cellular connectivity, mobile financial services adoption, and smartphone penetration, which together create the foundation for mobile-first gaming behavior.

The Formats Reshaping Mobile Engagement

Before diving into market dynamics and regulatory constraints, it helps to understand what instant win and crash games actually are and why they fit Bangladesh's mobile usage patterns so precisely.

Crash games follow a structurally simple loop: place a bet, watch a multiplier rise in real time, decide when to cash out. If the game crashes before you cash out, your stake is lost. The entire experience unfolds on a single screen, with a single decision. Aviator, JetX, Spaceman, Space XY, and Crash X are the titles appearing most frequently in Bangladesh-facing content. The format works because it removes decision layers and reduces interaction to a single action loop. There are no multi-step decisions, no rule variations to learn, and no strategic depth that requires desktop screen real estate.

Instant win games cover a broader category: Mines, Plinko, scratchcards, keno, and dice. All share the same design philosophy. Sessions are fast. Outcomes are immediate. The user experience is optimized for single-hand, vertical-screen interaction. Hacksaw Gaming explicitly markets its scratchcard portfolio as "completely optimized for mobile devices in vertical mode," which is exactly how Bangladeshi users interact with their phones throughout the day in short, repeated sessions.

These formats align with measurable mobile behavior patterns. Average crash game sessions globally run 12-16 minutes according to tracking data we reviewed, which is long enough to monetize through multiple rounds but short enough to fit micro-sessions that characterize mobile entertainment consumption. Decision frequency is high—players complete more rounds per minute than traditional table games—and engagement tooling like leaderboards, public bet histories, chat feeds, and multiplier displays adds social proof that drives virality and repeat access.

From a product design perspective, the logic is straightforward. If you are building for a market where 73.2% of mobile connections are broadband-capable, smartphone household penetration exceeds 70%, and the median user age is 26, you optimize for vertical screens, thumb-friendly controls, and instant gratification. Crash and instant win formats deliver all three.

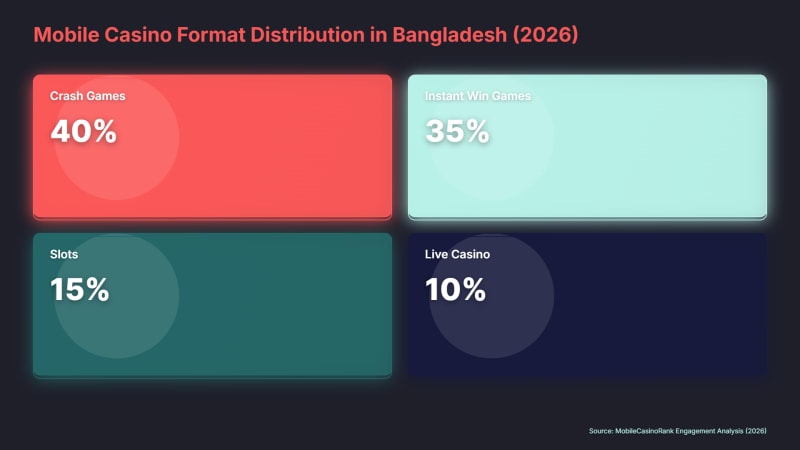

This chart shows the distribution of mobile casino formats in Bangladesh, highlighting the dominant share of crash and instant win games compared to traditional casino categories.

The engagement mechanics are intentional. They are extended through social layers—chat feeds showing other players' cashout decisions, recent multiplier displays that create FOMO, and leaderboards ranking top performers—that mirror the psychological hooks familiar to anyone who has used social media. Bangladesh had 64.0 million social media user identities as of October 2025, indicating a high baseline level of familiarity with feed-based UX and public performance metrics. Crash games leverage identical mechanics in a gambling context.

RTP positioning also plays a role in perceived fairness. Crash and instant formats often advertise high return-to-player percentages: Aviator at 97%, JetX at 96.70%, Spaceman at 96.60%, Plinko at 99%. Some titles implement provably fair cryptographic systems, allowing players to verify outcomes after the fact using published hash seeds, thereby adding a technical transparency layer that appeals to trust-sensitive users in markets with absent regulatory oversight.

However, high RTP does not mean low risk. Volatility remains high, session design structurally encourages chasing behavior through rapid round cycles, and "one more round" dynamics are embedded in the format itself. The simplicity that makes these games mobile-fit also makes them efficient at driving repeated engagement, which elevates addiction risk in jurisdictions without strong consumer protection frameworks or mandatory responsible gambling tooling.

The Legal Environment: Not Gray, Restrictive

Bangladesh's legal position on online gambling is unambiguous and increasingly operationalized through enforcement mechanisms targeting both access and payments.

The foundational prohibition framework derives from the Public Gambling Act of 1867, which remains in force and is routinely cited in court proceedings and regulatory guidance as the baseline restriction on gambling. The Penal Code of 1860 includes provisions such as Section 294A targeting unauthorized lottery offices, which matters operationally because many instant-win products use lottery-like user-experience patterns even when technically implemented as random-number-generator casino games.

The Cyber Security Ordinance 2025 represents a major enforcement inflection point. Section 20 explicitly criminalizes creating or operating a portal, app, or device for gambling purposes, participating in online gambling, assisting or encouraging participation, and advertising or promoting gambling directly or indirectly. Penalties include up to 2 years' imprisonment and fines of up to Tk 1 crore. This statutory language is especially relevant to crash and instant-win games because these formats are heavily marketed through affiliate networks, social media channels, and influencer partnerships.

That statute is not dormant paper law. In July 2023, the High Court directed BTRC to block online betting and gambling advertisements on digital platforms immediately and ordered Bangladesh Bank to issue directives to mobile financial service providers, including bKash and Nagad, to stop processing payments for betting websites. On network enforcement, BTRC blocking actions have been documented repeatedly. A 2022 report indicated that BTRC blocked 331 betting sites and reported gambling app and website links to Google, Facebook, and YouTube, with some removals confirmed after platform reviews.

This chart shows the contrast between the scale of mobile payment infrastructure and the increasing regulatory enforcement targeting gambling-related transactions.

In November 2025, the Bangladesh Bank escalated payment enforcement. An urgent directive to all mobile financial service providers mandated the immediate cessation of financial transactions linked to online gambling. The directive included specific compliance requirements: lists of suspicious accounts, dedicated anti-gambling task forces, AI-based transaction-monitoring systems designed to flag gambling-related flows, and public reporting mechanisms, including portals and helplines for user complaints.

The practical implication is clear. Even if offshore casinos remain accessible via mirror domains, VPN tunneling, or alternative DNS resolution, deposit and withdrawal friction becomes the binding constraint for mass-market mobile users who depend on bKash, Nagad, or Rocket rather than international credit cards or cryptocurrency wallets. The enforcement model is not primarily about blocking access. It is about choking payments, a higher-leverage intervention point for disrupting offshore gambling ecosystems that require local-currency on-ramps.

The Infrastructure Enabling Mobile Adoption

The regulatory environment is restrictive, and enforcement is operational, but the infrastructure that would theoretically enable mobile casino adoption at scale exists and is mature.

Bangladesh had 186 million cellular mobile connections at the end of 2025, representing 105% of the population. Internet users totaled 82.8 million, representing 47% penetration, and 73.2% of mobile connections were broadband-capable via 3G, 4G, or 5G networks.

Smartphone penetration is rising and measurable through household survey data. Bangladesh Bureau of Statistics reporting from the ICT Access and Use Survey covering Q1 FY26 indicates the share of households using smartphones climbed from 63.3% in 2023 to 72.8% in FY25 and 72.4% in Q1 FY26. Household internet access reached 56.2% in the same period.

The payments infrastructure is where Bangladesh's mobile ecosystem truly stands out. Mobile financial services are massive in absolute and relative terms. As of January 2025, Bangladesh had 239.3 million MFS accounts, up from 219.12 million in January 2024, with a monthly transaction volume of Tk 1.72 trillion. bKash alone reports a customer base exceeding 82 million as of December 2025 and operates under Bangladesh Bank regulation.

However, that same infrastructure is now the primary enforcement surface. Bangladesh Bank's November 2025 directive requiring MFS providers to halt gambling-linked transactions and implement AI-based detection, suspicious account monitoring, and dedicated task forces means the "local wallet convenience" frequently cited in mobile casino marketing materials is structurally vulnerable to regulatory intervention.

Demographics reinforce the mobile-first consumption thesis. Bangladesh's median age is 26, supporting the hypothesis that entertainment products resembling casual mobile games can scale faster than complex, strategy-heavy table games, especially when localized. Some instant-win games already offer Bengali-language options, which reduces friction for non-English-fluent users.

Why Crash and Instant Win Games Fit Bangladesh

The alignment between crash/instant formats and Bangladesh's mobile usage conditions is not coincidental. It reflects three structural product-market fits.

- The design of these formats matches how people actually use their phones. As mentioned, crash games and instant win formats are architected for vertical screens, single-hand thumb interaction, and immediate outcome delivery. Bangladeshi internet users access the web primarily via mobile devices, often in short bursts distributed throughout the day during commutes, work breaks, and idle moments. The format matches the behavior.

- Low-friction onboarding eliminates learning barriers. Crash game mechanics are simple enough that mobile interfaces do not require tutorial overlays, multi-step onboarding flows, or rule explanation screens. A new player can join a live table and place a first bet within seconds of opening the app. In a market where attention windows are short and competition for screen time is intense, reducing time-to-first-action is a structural competitive advantage.

- High-frequency session design with embedded social hooks. This includes real-time chat feeds, public bet histories that create social proof, leaderboards that rank performance, and recent multiplier displays that generate FOMO. Bangladesh had 64.0 million social media user identities as of October 2025, indicating high baseline comfort with feed-based interfaces.

Market Size: What Can Be Measured, What Remains Modeled

Bangladesh does not publish official regulated online gambling market data because online gambling operates in a restricted legal environment without licensing infrastructure. Consequently, market size estimates rely on offshore operators' signals, payment-flow proxies, and third-party forecasting models.

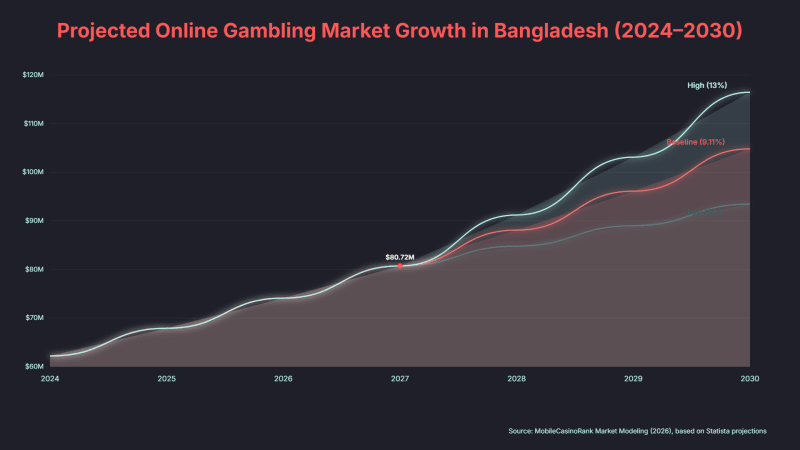

A widely cited anchor comes from a LiveCasinoRank press release referencing Statista projections indicating Bangladesh's online gambling market could reach US$80.72 million by 2027, reflecting a compound annual growth rate of 9.11% from 2024 to 2027. That figure appears across multiple affiliate and industry press contexts. It is plausible as an order-of-magnitude estimate for offshore-served gray market activity. Still, it should be explicitly labeled as a third-party forecast rather than measured market data.

If we assume mobile accounts for 70-90% of Bangladesh's online gambling activity—a reasonable range given mobile-first internet access patterns and smartphone household penetration above 70%—the implied mobile gambling market volume in 2027 would range from approximately US$56.5 million at 70% mobile share to US$72.65 million at 90% mobile share.

Projecting forward to 2030 using three CAGR scenarios—5% representing conservative growth under intensified enforcement, 9.11% representing baseline continuation, and 13% representing accelerated adoption if enforcement stabilizes—the total online market volume could range from US$93.45 million in the low scenario to US$116.47 million in the high scenario.

For comparative context, Grand View Research estimates India's online gambling market could reach US$10.78 billion by 2030 with a 13.7% CAGR. Global Market Insights projects the global online gambling market will grow from US$95.5 billion in 2024 to US$257 billion by 2034 at a 10.5% CAGR.

Bangladesh's forecast market size is small in absolute dollar terms. Still, it is strategically noteworthy because mobile and mobile money infrastructure are already mature, and instant, crash-based formats match local device usage and attention patterns. Demographic tailwinds create conditions for rapid adoption if regulatory constraints were to loosen. The binding constraint is not infrastructure or product-market fit. It is the legal framework and enforcement intensity, both of which are tightening rather than easing through 2025 and into early 2026.

The Risks Shaping Market Reality

Bangladesh's mobile casino opportunity cannot be separated from its risk surface. For operators, publishers, and users, the risks are structural, measurable, and accelerating.

- Legal and regulatory risk is the most visible and carries direct statutory exposure. Gambling is restricted under foundational law, and online gambling is explicitly criminalized under the Cyber Security Ordinance 2025 Section 20, which includes penalties for creating, operating, participating in, and advertising gambling platforms. Enforcement includes court-backed ISP blocking coordinated by the BTRC, payment rail disruption mandated by Bangladesh Bank directives to MFS providers, and platform-level takedowns in which Google, Facebook, and YouTube remove flagged gambling apps and links in response to regulatory complaints.

- Fraud and scam risk escalates sharply in restricted markets where users are pushed toward mirror domains, unofficial app stores, and APK sideloading. Phishing sites mimicking legitimate casino brands, fake apps embedding malware, and "predictor scams" promising algorithmic advantages proliferate in environments where users cannot access verified app stores or rely on regulatory vetting.

- Addiction and harm risk are structurally elevated by crash and instant-win format design characteristics. Rapid round cycles enable high decision frequency, which accelerates loss velocity for users employing chase strategies. Simple mechanics reduce cognitive load, making it psychologically easier to play reflexively. Mobile accessibility means gambling is always within reach, removing natural friction points that might otherwise limit play frequency.

- Payment and AML exposure are heightened by regulatory and press narratives linking online gambling to illicit financial flows. Bangladesh Bank's November 2025 directive requiring MFS providers to implement suspicious account lists, dedicated anti-gambling task forces, and AI-based transaction monitoring reflects intensified anti-money-laundering scrutiny specifically targeting gambling flows.

What the Data Tells Us About 2026

The trajectory entering 2026 is not toward liberalization or regulatory ambiguity. It is toward more sophisticated, data-driven, multi-layered enforcement targeting both access and payments simultaneously.

BTRC's blocking actions are no longer limited to one-time domain lists. They are ongoing, responsive operations that target mirror sites and workaround domains as they appear. Bangladesh Bank's MFS directive is not advisory guidance. It includes specific operational requirements that shift MFS providers from passive payment processors to active compliance gatekeepers with measurable obligations.

This chart shows projected growth scenarios for Bangladesh’s online gambling market through 2030, based on varying assumptions around enforcement and adoption rates.

The format landscape is also evolving. Crash and instant-win games will continue to gain share of mobile casino visibility, not because regulatory pressure is easing, but because their product design advantages compound in attention-scarce markets regardless of legal status. The better these formats perform at capturing and monetizing attention, the more enforcement scrutiny they will attract.

For operators, the strategic question is not "can we access this market" but "should we," and the answer increasingly depends on risk appetite for legal exposure, reputational damage, payment disruption, and enforcement volatility. For users, the risk is not just legal but operational: fraud, scams, unregulated products, and the absence of consumer protection mechanisms.

The infrastructure is already in place, and the audience is reachable. The limiting factor is enforcement.